Ex. 99.2

Solicitation Version

|

§

|

|||

|

In re:

|

§

|

Chapter 11

|

|

|

§

|

|||

|

LUMINAR TECHNOLOGIES, INC.,

|

§

|

Case No. 25-90807 (CML)

|

|

|

et al.,

|

§

|

||

|

Debtors.1

|

§

|

(Jointly Administered)

|

|

|

§

|

|||

|

§

|

DISCLOSURE STATEMENT FOR

THIRD AMENDED CHAPTER 11 PLAN OF LIQUIDATION OF

THIRD AMENDED CHAPTER 11 PLAN OF LIQUIDATION OF

LUMINAR TECHNOLOGIES, INC. AND ITS AFFILIATED DEBTORS

|

WEIL, GOTSHAL & MANGES LLP

Stephanie N. Morrison (24126930) Austin B. Crabtree (24109763)

700 Louisiana Street, Suite 3700

Houston, Texas 77002

Telephone: (713) 546-5000

Facsimile: (713) 224-9511

|

WEIL, GOTSHAL & MANGES LLP

Ronit J. Berkovich (admitted pro hac vice) Jessica Liou (admitted pro hac vice) 767 Fifth Avenue New York, New York 10153 Telephone: (212) 310-8000 Facsimile: (212) 310-8007 |

|

Attorneys for Debtors and Debtors in Possession

|

|

|

Dated: February 18, 2026

Houston, Texas |

|

1

|

The Debtors in these chapter 11 cases, along with the last four digits of each Debtor’s federal tax identification number, are as follows: LAZR Technologies, LLC (8909); Luminar Technologies, Inc. (4317);

Luminar, LLC (7133); Condor Acquisition Sub I, Inc. (0155); and Condor Acquisition Sub II, Inc. (8587). The Debtors’ mailing address is 2603 Discovery Drive, Suite 100, Orlando, Florida 32826.

|

THIS SOLICITATION OF VOTES (THE “SOLICITATION”) IS BEING CONDUCTED TO OBTAIN SUFFICIENT VOTES TO ACCEPT THE PLAN (AS DEFINED HEREIN).

THE DEADLINE TO ACCEPT OR REJECT THE PLAN IS 4:00 P.M. (CENTRAL TIME) ON MARCH 23, 2026 (THE “VOTING DEADLINE”), UNLESS EXTENDED BY THE DEBTORS IN WRITING.

THE RECORD DATE FOR DETERMINING WHICH HOLDERS OF CLAIMS MAY VOTE ON THE PLAN IS FEBRUARY 18, 2026 (THE “RECORD DATE”).

RECOMMENDATION BY THE DEBTORS TO VOTE TO ACCEPT THE PLAN

The board of directors of each of Luminar Technologies, Inc., Condor Acquisition Sub I, Inc., and Condor Acquisition Sub II, Inc. and the sole member of each of LAZR Technologies, LLC and Luminar, LLC have

approved the transactions contemplated by the Plan. The Debtors believe the Plan is in the best interests of all stakeholders and recommend that all creditors whose votes are being solicited submit ballots to accept the Plan.

RECOMMENDATION BY THE CREDITORS’ COMMITTEE

TO VOTE TO ACCEPT THE PLAN

The Creditors’ Committee (i) believes that the Plan is in the best interests of the Debtors’ general unsecured creditors, (ii) supports confirmation of the Plan and (iii) recommends that all general unsecured

creditors in Class 5 submit a ballot to accept the Plan.

THE INFORMATION CONTAINED IN THIS DISCLOSURE STATEMENT (AS MAY BE AMENDED, SUPPLEMENTED, OR MODIFIED FROM TIME TO TIME, THE “DISCLOSURE STATEMENT”) IS INCLUDED HEREIN FOR THE PURPOSES OF

SOLICITING VOTES ON THE THIRD AMENDED CHAPTER 11 PLAN OF LIQUIDATION OF LUMINAR TECHNOLOGIES, INC. AND ITS AFFILIATED DEBTORS, DATED FEBRUARY 18, 2026 (THE “PLAN”),2 AND MAY NOT BE RELIED UPON FOR ANY PURPOSE OTHER THAN TO DETERMINE HOW TO VOTE ON THE PLAN. A COPY OF THE PLAN IS ANNEXED HERETO AS EXHIBIT A. NO SOLICITATION OF VOTES TO ACCEPT OR REJECT THE

PLAN MAY BE MADE EXCEPT PURSUANT TO SECTION 1125 OF CHAPTER 11 OF TITLE 11 OF THE UNITED STATES CODE (THE “BANKRUPTCY CODE”).

| 2 |

Capitalized terms used but not otherwise defined herein shall have the meanings ascribed to such terms in the Plan.

|

ii

ALL HOLDERS OF CLAIMS AND INTERESTS ARE ADVISED AND ENCOURAGED TO READ THE DISCLOSURE STATEMENT AND THE PLAN IN THEIR ENTIRETY BEFORE VOTING TO ACCEPT OR REJECT THE PLAN. IN PARTICULAR, ALL

HOLDERS OF CLAIMS AND INTERESTS SHOULD CAREFULLY READ AND CONSIDER FULLY THE RISK FACTORS SET FORTH IN SECTION VI (CERTAIN RISK FACTORS AFFECTING DEBTORS) OF THIS DISCLOSURE STATEMENT BEFORE VOTING TO ACCEPT OR REJECT THE PLAN. THE PLAN SUMMARIES

AND STATEMENTS MADE IN THIS DISCLOSURE STATEMENT ARE QUALIFIED IN THEIR ENTIRETY BY REFERENCE TO THE PLAN AND THE EXHIBITS ANNEXED TO THE PLAN AND THIS DISCLOSURE STATEMENT. IN THE EVENT OF ANY CONFLICT BETWEEN THE DESCRIPTIONS SET FORTH IN THIS

DISCLOSURE STATEMENT AND THE TERMS OF THE PLAN, THE TERMS OF THE PLAN GOVERN.

THE DISCLOSURE STATEMENT HAS BEEN PREPARED IN ACCORDANCE WITH SECTION 1125 OF THE BANKRUPTCY CODE AND RULE 3016(b) OF THE FEDERAL RULES OF BANKRUPTCY PROCEDURE (THE “BANKRUPTCY RULES”) AND

NOT NECESSARILY IN ACCORDANCE WITH OTHER NON-BANKRUPTCY LAW.

HOLDERS OF CLAIMS AND INTERESTS SHOULD NOT CONSTRUE THE CONTENTS OF THE DISCLOSURE STATEMENT AS PROVIDING ANY LEGAL, BUSINESS, FINANCIAL, OR TAX ADVICE AND SHOULD CONSULT WITH THEIR OWN ADVISORS

BEFORE CASTING A VOTE WITH RESPECT TO THE PLAN.

CERTAIN STATEMENTS CONTAINED IN THE DISCLOSURE STATEMENT, INCLUDING STATEMENTS INCORPORATED BY REFERENCE, PROJECTED FINANCIAL INFORMATION, AND OTHER FORWARD-LOOKING STATEMENTS, ARE BASED ON

ESTIMATES AND ASSUMPTIONS. THERE CAN BE NO ASSURANCE THAT SUCH STATEMENTS WILL BE REFLECTIVE OF ACTUAL OUTCOMES. FORWARD-LOOKING STATEMENTS SHOULD BE EVALUATED IN THE CONTEXT OF THE ESTIMATES, ASSUMPTIONS, UNCERTAINTIES, AND RISKS DESCRIBED

HEREIN.

FURTHERMORE, READERS ARE CAUTIONED THAT ANY FORWARD-LOOKING STATEMENTS HEREIN, INCLUDING ANY PROJECTIONS, ARE SUBJECT TO A NUMBER OF ASSUMPTIONS, RISKS, AND UNCERTAINTIES, MANY OF WHICH ARE BEYOND

THE CONTROL OF THE DEBTORS, INCLUDING THE IMPLEMENTATION OF THE PLAN. IMPORTANT ASSUMPTIONS AND OTHER IMPORTANT FACTORS THAT COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY INCLUDE THOSE FACTORS, RISKS, AND UNCERTAINTIES DESCRIBED IN MORE DETAIL

UNDER THE HEADING “CERTAIN RISK FACTORS AFFECTING DEBTORS” BELOW. PARTIES ARE CAUTIONED THAT THE FORWARD-LOOKING STATEMENTS SPEAK AS OF THE DATE MADE, ARE BASED ON THE DEBTORS’ CURRENT BELIEFS, INTENTIONS, AND EXPECTATIONS, AND ARE NOT GUARANTEES

OF FUTURE PERFORMANCE. ACTUAL RESULTS OR DEVELOPMENTS MAY DIFFER MATERIALLY FROM THE EXPECTATIONS EXPRESSED OR IMPLIED IN THE FORWARD-LOOKING STATEMENTS, AND THE DEBTORS UNDERTAKE NO OBLIGATION TO UPDATE ANY SUCH STATEMENTS. THE DEBTORS DO NOT

INTEND, AND UNDERTAKE NO OBLIGATION, TO UPDATE OR OTHERWISE REVISE ANY FORWARD-LOOKING STATEMENTS, INCLUDING ANY PROJECTIONS CONTAINED HEREIN, TO REFLECT EVENTS OR CIRCUMSTANCES EXISTING OR ARISING AFTER THE DATE HEREOF OR TO REFLECT THE OCCURRENCE

OF UNANTICIPATED EVENTS OR OTHERWISE.

NO INDEPENDENT AUDITOR OR ACCOUNTANT HAS REVIEWED OR APPROVED THE LIQUIDATION ANALYSIS HEREIN. THE STATEMENTS CONTAINED IN THE DISCLOSURE STATEMENT ARE MADE AS OF THE DATE HEREOF UNLESS OTHERWISE

SPECIFIED.

iii

THE DEBTORS HAVE NOT AUTHORIZED ANY PERSON TO GIVE ANY INFORMATION OR ADVICE, OR TO MAKE ANY REPRESENTATION, IN CONNECTION WITH THE PLAN OR THE DISCLOSURE STATEMENT.

THE INFORMATION IN THE DISCLOSURE STATEMENT IS BEING PROVIDED SOLELY FOR PURPOSES OF VOTING TO ACCEPT OR REJECT THE PLAN OR OBJECTING TO CONFIRMATION. NOTHING IN THE DISCLOSURE STATEMENT MAY BE

USED BY ANY PARTY FOR ANY OTHER PURPOSE.

ALL EXHIBITS TO THE DISCLOSURE STATEMENT ARE INCORPORATED INTO AND ARE A PART OF THE DISCLOSURE STATEMENT AS IF SET FORTH IN FULL HEREIN.

THE PLAN PROVIDES THAT THE FOLLOWING PARTIES ARE DEEMED TO GRANT THE RELEASES PROVIDED FOR THEREIN: (A) THE DEBTORS; (B) THE CREDITORS’ COMMITTEE AND EACH OF ITS MEMBERS, SOLELY IN THEIR CAPACITIES AS SUCH; (C) THE AD HOC NOTEHOLDER GROUP; (D) THE FIRST LIEN NOTES AGENT AND

SECOND LIEN NOTES AGENT, SOLELY IN THEIR CAPACITIES AS SUCH; AND (E) WITH RESPECT TO EACH OF THE FOREGOING PERSONS IN CLAUSES (A) THROUGH (D), ALL RELATED PARTIES; (F) THE HOLDERS OF ALL CLAIMS OR INTERESTS WHOSE VOTE TO ACCEPT OR REJECT THE PLAN

IS SOLICITED BUT THAT DO NOT VOTE EITHER TO ACCEPT OR TO REJECT THE PLAN AND DO NOT OPT OUT OF GRANTING THE RELEASES SET FORTH IN ARTICLE XI OF THE PLAN; (G) THE HOLDERS OF ALL CLAIMS OR INTERESTS THAT VOTE TO ACCEPT OR REJECT THE PLAN, ARE

DEEMED TO REJECT THE PLAN, OR ARE PRESUMED TO ACCEPT THE PLAN, BUT IN EACH CASE DO NOT OPT OUT OF GRANTING THE RELEASES SET FORTH IN ARTICLE XI OF THE PLAN; (H) THE HOLDERS OF ALL CLAIMS AND INTERESTS THAT WERE GIVEN NOTICE OF THE OPPORTUNITY TO

OPT OUT OF GRANTING THE RELEASES SET FORTH IN SECTION 11.6 OF THE PLAN BUT DID NOT OPT OUT.

HOLDERS OF CLAIMS OR INTERESTS IN VOTING CLASSES (CLASS 3 (FIRST LIEN NOTEHOLDER SECURED CLAIMS), CLASS 4 (SECOND LIEN NOTEHOLDER SECURED CLAIMS), AND CLASS 5 (GENERAL UNSECURED

CLAIMS)) WILL RECEIVE A BALLOT THAT INCLUDES THE OPTION TO OPT OUT OF THE RELEASES CONTAINED IN SECTION 11.6 OF THE PLAN. HOLDERS OF CLAIMS AND INTERESTS IN CERTAIN

NON-VOTING CLASSES (CLASS 1 (OTHER PRIORITY CLAIMS), CLASS 2 (OTHER SECURED CLAIMS), CLASS 8 (SUBORDINATED CLAIMS), AND CLASS 9 (PARENT INTERESTS)) WILL RECEIVE A NOTICE OF NON-VOTING STATUS THAT (I) NOTIFIES SUCH HOLDERS OF THEIR RIGHT TO OPT

OUT OF THE RELEASES CONTAINED IN SECTION 11.6 OF THE PLAN AND (II) INCLUDES A FORM PURSUANT TO WHICH SUCH HOLDERS CAN OPT OUT OF THE RELEASES CONTAINED IN SECTION 11.6 OF THE PLAN. SEE EXHIBIT D FOR A DESCRIPTION OF THE RELEASES AND

RELATED PROVISIONS.

PLEASE BE ADVISED THAT SECTIONS 11.3, 11.4, 11.5, 11.6, 11.7, 11.8, AND 11.9 OF THE PLAN CONTAIN RELEASE, EXCULPATION, AND INJUNCTION PROVISIONS. YOU SHOULD REVIEW AND CONSIDER THE PLAN CAREFULLY

BECAUSE YOUR RIGHTS MAY BE AFFECTED.

iv

NEITHER (A) THE ISSUANCE NOR THE DISTRIBUTION OF THE PARENT DEBTOR ADDITIONAL STOCK, NOR (B) THE ISSUANCE OF THE LIQUIDATING TRUST INTERSETS HAVE BEEN APPROVED OR DISAPPROVED BY THE SECURITIES AND

EXCHANGE COMMISSION (THE “SEC”) OR BY ANY STATE SECURITIES COMMISSION OR OTHER PUBLIC, GOVERNMENTAL, OR REGULATORY AUTHORITY, AND NEITHER THE SEC NOR ANY SUCH AUTHORITY HAS PASSED UPON THE ACCURACY OR

ADEQUACY OF THE INFORMATION CONTAINED IN THIS DISCLOSURE STATEMENT OR UPON THE MERITS OF THE PLAN OR THE ISSUANCE AND THE DISTRIBUTION OF THE PARENT DEBTOR ADDITIONAL STOCK. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

An opt-out election form (the “Release Opt-Out Form”) or a Ballot (as defined herein) containing an opt-out election has been or will be mailed to you. The Release

Opt-Out Form or Ballot, as applicable, will provide you with the option to opt out of granting the releases contained in Section 11.6(b) of the Plan. You must complete and timely return the Release Opt-Out Form or Ballot, as applicable, to the

Voting Agent (as defined herein) by the Voting Deadline, March 23, 2026 at 4:00 p.m. (Central Time), in accordance with the instructions set forth in the Release Opt-Out Form or Ballot, as applicable, for your opt-out to be valid. OTHERWISE,

EXCEPT AS EXPRESSLY SET FORTH IN THE PLAN, YOU WILL BE DEEMED TO CONSENT TO AND BE BOUND BY THE RELEASES SET FORTH IN THE PLAN. Please review the additional information set forth in this Disclosure Statement, the Plan, the Release Opt-Out Form,

and the Ballot, as applicable, and any other documents related to these chapter 11 cases that you may receive from time to time. Please be advised that your decision to opt out or not opt out of the releases in Section 11.6(b) of the Plan does

not affect the amount of any distribution you may receive under the Plan.

v

|

I. INTRODUCTION

|

10

|

|||

|

A.

|

OVERVIEW OF PLAN

|

11

|

||

|

B.

|

GLOBAL SETTLEMENT

|

13

|

||

|

C.

|

TREATMENT OF CLAIMS AND INTERESTS

|

15

|

||

|

1.

|

Claims and Interests in Luminar Technologies, Inc.

|

15

|

||

|

2.

|

Key Recovery Table Assumptions and Qualifications

|

17

|

||

|

D.

|

VOTING PROCEDURES

|

18

|

||

|

II. OVERVIEW OF DEBTORS’ OPERATIONS

|

19

|

|||

|

A.

|

COMPANY’S BACKGROUND AND FORMATION

|

19

|

||

|

B.

|

BUSINESS OPERATIONS

|

21

|

||

|

1.

|

LiDARCo

|

21

|

||

|

2.

|

LSICo

|

22

|

||

|

C.

|

CORPORATE STRUCTURE AND GOVERNANCE

|

23

|

||

|

1.

|

Corporate Structure

|

23

|

||

|

2.

|

Capital Structure

|

24

|

||

|

a.

|

First Lien Notes

|

24

|

||

|

b.

|

Second Lien Convertible Notes

|

25

|

||

|

c.

|

Intercreditor Agreement

|

25

|

||

|

d.

|

Unsecured Convertible Notes

|

26

|

||

|

e.

|

Additional Financing Agreements (No Amounts Outstanding)

|

26

|

||

|

f.

|

Common Stock

|

27

|

||

|

3.

|

Prepetition Litigation

|

27

|

||

|

a.

|

Securities Class Action (2023 Action)

|

27

|

||

|

b.

|

Securities Class Action (2025 Action)

|

27

|

||

|

c.

|

Shareholder Derivative Suits (2023)

|

28

|

||

|

d.

|

Shareholder Derivative Suit (2025)

|

28

|

||

|

e.

|

SEC Investigation

|

28

|

||

|

f.

|

Solfice Shareholder Suit (2025)

|

29

|

||

| 4. |

Liquidity

|

29

|

||

| 5. |

Other Assets

|

29

|

||

|

III. KEY EVENTS LEADING TO COMMENCEMENT OF CHAPTER 11 CASES

|

29

|

|||

|

A.

|

CHALLENGES FACING THE DEBTORS’ BUSINESSES

|

30

|

||

vi

|

1.

|

Volvo Relationship Deterioration

|

30

|

|

|

2.

|

Consequences of Partnership Setbacks

|

31

|

|

|

3.

|

Industry Challenges

|

32

|

|

|

B.

|

FINANCIAL PERFORMANCE

|

33

|

|

|

C.

|

LIABILITY MANAGEMENT AND CAPITAL RAISING INITIATIVES

|

33

|

|

|

D.

|

KEY EMPLOYEE RETENTION PROGRAM

|

34

|

|

|

E.

|

OPERATIONAL RESTRUCTURING EFFORTS

|

35

|

|

|

F.

|

PURSUIT OF STRATEGIC AND SALE TRANSACTIONS

|

35

|

|

|

IV. KEY EVENTS DURING CHAPTER 11 CASES

|

37

|

||

|

A.

|

FIRST DAY PLEADINGS

|

37

|

|

|

B.

|

CASH COLLATERAL

|

38

|

|

|

C.

|

COST-SAVING MEASURES

|

39

|

|

|

D.

|

FILING OF CONDOR ENTITIES

|

39

|

|

|

E.

|

ADDITIONAL MOTIONS AND APPLICATIONS

|

39

|

|

|

F.

|

TIMETABLE FOR CHAPTER 11 CASES

|

40

|

|

|

G.

|

GLOBAL BIDDING PROCEDURES AND POSTPETITION SALE PROCESS

|

40

|

|

|

1.

|

LSI Assets Sale Process

|

41

|

|

|

2.

|

LiDAR Assets Sale Process

|

41

|

|

|

3.

|

Asset Sale Offer

|

43

|

|

|

H.

|

STATEMENTS AND SCHEDULES, AND CLAIMS BAR DATES

|

43

|

|

|

I.

|

ADVERSARY PROCEEDINGS

|

44

|

|

|

1.

|

Puttagunta Adversary Proceeding

|

44

|

|

|

2.

|

NEXT Semiconductor Technologies, Inc. Adversary Proceeding

|

45

|

|

|

J.

|

SIC INVESTIGATION

|

45

|

|

|

K.

|

CREDITORS’ COMMITTEE INVESTIGATION

|

46

|

|

|

L.

|

COMMON STOCK

|

46

|

|

|

V. SECURITIES LAWS EXEMPTIONS AND RESTRICTIONS ON TRANSFER

|

47

|

||

|

VI. CERTAIN RISK FACTORS AFFECTING DEBTORS

|

47

|

||

|

A.

|

CERTAIN BANKRUPTCY LAW CONSIDERATIONS

|

47

|

|

|

1.

|

Risk Related to Termination of Consensual Use of Cash Collateral

|

47

|

|

|

2.

|

Risk of Non-Confirmation of Plan

|

48

|

|

|

3.

|

Risk of Non-Consensual Confirmation

|

48

|

|

|

4.

|

Risk of Non-Occurrence of Effective Date

|

48

|

|

|

5.

|

Alternative Transactions

|

48

|

|

|

6.

|

Risks Related to Possible Objections to Plan

|

49

|

|

vii

|

7.

|

Global Settlement May Not Be Approved

|

49

|

|

|

8.

|

Releases, Injunctions, and Exculpation Provisions May Not Be Approved

|

49

|

|

|

9.

|

Claims Could Be More than Projected

|

49

|

|

|

10.

|

Participation in the Asset Sale Offer Could be Less Than Anticipated

|

49

|

|

|

11.

|

Distributions

|

49

|

|

|

12.

|

Administrative Insolvency

|

50

|

|

|

13.

|

Conversion to Chapter 7

|

50

|

|

|

14.

|

The Debtors’ Liquidity May be Exhausted and No Alternative Financing may be Obtained Before the Effective Date

|

50

|

|

|

15.

|

Dismissal of Chapter 11 Cases

|

50

|

|

|

16.

|

Cost of Administering Debtors’ Estates

|

50

|

|

|

B.

|

ADDITIONAL FACTORS TO BE CONSIDERED

|

51

|

|

|

1.

|

Debtors Could Withdraw Plan

|

51

|

|

|

2.

|

Debtors Have No Duty to Update

|

51

|

|

|

3.

|

No Representations Outside This Disclosure Statement Are Authorized

|

51

|

|

|

4.

|

No Legal or Tax Advice Is Provided to You by This Disclosure Statement

|

51

|

|

|

5.

|

No Admission Made

|

51

|

|

|

6.

|

No Waiver of Right to Object or Right to Recover Transfers and Assets

|

51

|

|

|

7.

|

Ongoing Litigation Could Affect the Outcome of the Chapter 11 Cases

|

52

|

|

|

8.

|

Objection to Amount or Classification of Claims

|

52

|

|

|

VII. CERTAIN U.S. FEDERAL INCOME TAX CONSEQUENCES

|

52

|

||

|

A.

|

CONSEQUENCES TO DEBTORS

|

53

|

|

|

1.

|

Transfer of Assets to the Liquidation Trust; Wind Down of the Debtors

|

54

|

|

|

2.

|

Cancellation of Debt

|

54

|

|

|

B.

|

CONSEQUENCES TO HOLDERS OF ALLOWED GENERAL UNSECURED CLAIMS

|

55

|

|

|

1.

|

Treatment to U.S. Holders of Allowed First Lien Noteholder Secured Claims or Allowed Second Lien Secured Claims

|

55

|

|

|

2.

|

Treatment to U.S. Holders of Allowed General Unsecured Claims

|

56

|

|

|

3.

|

Distributions in Respect of Accrued But Unpaid Interest or OID

|

57

|

|

|

4.

|

Character of Gain or Loss

|

58

|

|

|

C.

|

TAX TREATMENT OF LIQUIDATION TRUST AND ITS BENEFICIARIES

|

58

|

|

|

1.

|

General “Liquidating Trust” Tax Reporting by the Liquidation Trust and their Beneficiaries

|

59

|

|

viii

|

2.

|

Tax Reporting for Assets Allocable to a Disputed Ownership Fund (including the GUC Reserve)

|

60

|

||

|

D.

|

WITHHOLDING ON DISTRIBUTIONS AND INFORMATION REPORTING

|

60

|

||

|

VIII. CONFIRMATION OF PLAN

|

61

|

|||

|

A.

|

CONFIRMATION HEARING

|

61

|

||

|

B.

|

OBJECTIONS

|

61

|

||

|

C.

|

REQUIREMENTS FOR CONFIRMATION OF PLAN

|

62

|

||

|

1.

|

Requirements of Section 1129(a) of Bankruptcy Code

|

62

|

||

|

2.

|

Acceptance of Plan

|

63

|

||

|

3.

|

Cramdown

|

63

|

||

|

a.

|

No Unfair Discrimination

|

64

|

||

|

b.

|

Fair and Equitable Test

|

64

|

||

|

4.

|

Best Interests Test

|

65

|

||

|

5.

|

Feasibility

|

65

|

||

|

IX. RELEASES

|

65

|

|||

|

X. ALTERNATIVES TO CONFIRMATION AND CONSUMMATION OF PLAN

|

66

|

|||

|

1.

|

Alternative Plan of Liquidation

|

67

|

||

|

2.

|

Liquidation under Chapter 7 of Bankruptcy Code

|

67

|

||

|

XI. CONCLUSION

|

67

|

|||

|

EXHIBIT A

|

Plan [filed separately]

|

|

EXHIBIT B

|

Debtors’ Organizational Structure

|

|

EXHIBIT C

|

Liquidation Analysis

|

|

EXHIBIT D

|

Release, Injunction and Exculpation Provisions

|

|

EXHIBIT E

|

Solicitation and Voting Procedures

|

ix

On December 15, 2025, and December 31, 2025, as applicable (the “Petition Date”), Luminar Technologies, Inc. (“Luminar”

or “Luminar Parent”), LAZR Technologies, LLC, Luminar, LLC, Condor Acquisition Sub I, Inc., and Condor Acquisition Sub II, Inc. (together with Luminar, the “Debtors”,

and, the Debtors collectively with the Debtors’ direct and indirect non-debtor subsidiaries, the “Company”) commenced voluntary cases in the United States Bankruptcy Court for the Southern District of Texas

(the “Bankruptcy Court”) pursuant to chapter 11 of the Bankruptcy Code. The Debtors’ chapter 11 cases are being jointly administered for procedural purposes only pursuant to Bankruptcy Rule 1015(b).

On December 30, 2025, the United States Trustee for Region 7 (the “U.S. Trustee”) appointed the Creditors’ Committee pursuant to section 1102 of the

Bankruptcy Code to represent the interests of unsecured creditors in the chapter 11 cases (Docket No. 115). The members of the Creditors’ Committee are (i) U.S. Bank Trust Company, National Association, (ii) Fujian Hitronics Technologies, Inc.,

(iii) Applied Intuition, Inc., (iv) Optera TPK Holding Pte., Ltd. and TPK Precision Hong Kong Co., Ltd., (v) Workday, Inc., (vi) STEER Tech LLC, and (vii) Alidade Discovery Lakes, II, LLC. The Creditors’ Committee retained Paul Hastings LLP (“Paul Hastings”) as counsel and Alvarez & Marsal Holdings, LLC (A&M) as financial advisor.

The purpose of this Disclosure Statement is to provide information of a kind, and in sufficient detail, to enable creditors of the Debtors that are entitled to vote on the Plan to make an informed

decision on whether to vote to accept or reject the Plan. The Disclosure Statement contains, among other things, a summary of (i) the treatment of Claims against and Interests in the Debtors under the Plan, (ii) the Debtors’ business and certain

historical events, (iii) anticipated events during these chapter 11 cases, (iv) risk factors affecting the Debtors and the Plan, and (v) the standard for seeking confirmation of the Plan.

As described in more detail below, the Debtors faced certain financial difficulties prior to the Petition Date and commenced these chapter 11 cases to facilitate value-maximizing sale processes for

its LiDAR business and for the equity of Luminar Semiconductors Inc. (“LSI”) and certain of its subsidiaries (collectively, “LSICo”).

On December 15, 2025, the Debtors entered into a Stock Purchase Agreement with Quantum Computing, Inc. (“QCi”), the stalking horse bidder for the LSICo

equity. On December 18, 2025, the Debtors filed a motion seeking approval of bidding procedures, designation of QCi as the stalking horse bidder for the LSICo equity, and authorization to designate one or more stalking horse bidders for the

LiDARCo (as defined herein) equity (Docket No. 86) (the “Bidding Procedures Motion”), which was entered by the Bankruptcy Court on December 30, 2025 (Docket No. 119) (the “Bidding

Procedures Order”). The Debtors received no additional qualified bids, and the Bankruptcy Court approved the sale of the LSICo equity to QCi at a hearing held on January 27, 2026 (Docket No. 320). The LSI Sale Transaction closed on

February 2, 2026.

On January 11, 2026, the Debtors entered into a purchase agreement with QCi for the LiDARCo assets and filed a notice designating QCi as the stalking horse bidder for

the LiDARCo assets (Docket No. 202). The Debtors qualified an additional bid and held an auction for the LiDARCo assets on January 26, 2026. At the conclusion of the auction, the Debtors named MicroVision, Inc. (“MicroVision”)

as the successful bidder and QCi as the back-up bidder. At a hearing held on January 27, 2026, the Bankruptcy Court approved the sale of the LiDARCo assets to MicroVision (Docket No. 329). The LiDARCo Sale Transaction closed on February 3, 2026.

10

In the last several weeks, the Debtors have engaged in extensive negotiations with the Creditors’ Committee and Ad Hoc Noteholder Group, culminating in the entry into a global compromise and

settlement to resolve all of the Creditors’ Committee’s issues with the Plan, including the allocation of consideration to be distributed to holders of unsecured claims (the “Global Settlement”). The terms

of the Global Settlement are incorporated into the Plan and described in Section I.B herein.

| A. |

OVERVIEW OF PLAN

|

The Plan contemplates the distribution of the proceeds from the completed sales of substantially all the Debtors’ assets pursuant to section 363 of the Bankruptcy Code to QCi for LSICo and to

MicroVision for LiDARCo and the efficient and orderly wind-down of the Debtors’ estates in accordance with the Global Settlement.

To implement the provisions of the Plan, including making distributions to holders of Claims and Interests, the Plan contemplates the creation of a Liquidation Trust, as well as the appointment of

a Liquidation Trustee, the identity of which shall be included in the Plan Supplement. The selection of the Liquidation Trustee shall be mutually agreeable between the Ad Hoc Noteholder Group and the Creditors’ Committee, and reasonably acceptable

to the Debtors. The Liquidation Trustee shall carry out and implement all provisions of the Plan after the Effective Date, including the reconciliation of Claims, the monetization of the Liquidation Trust Assets, including the GUC Reserve Assets,

and the winding down of the Debtors’ estates. A Liquidation Trust Oversight Board shall be established to supervise the Liquidation Trustee’s reconciliation of General Unsecured Claims and its pursuit, abandonment, or liquidation of the GUC

Reserve Assets. The Liquidation Trust Oversight Board will be comprised of three (3) members, each of which will be selected by the Creditors’ Committee.

On or before the Effective Date, the Debtors and the Liquidation Trustee shall take all necessary steps to establish the Liquidation Trust for the benefit of Holders of Claims against the Debtors,

including executing the Liquidation Trust Agreement and the Liquidation Trust Transfer Agreement, each of which shall be in form and substance reasonably acceptable to the Debtors, the Required Senior Secured Holders, and the Creditors’ Committee,

and all of the Assets of the Debtors as of the Effective Date will vest with the Liquidation Trust.

The Plan further provides for, on the Effective Date, certain distributions to be made and reserves to be established, including (i) initial funding of the Senior Claims Reserve on account of

Allowed Administrative Expense Claims, Allowed Priority Tax Claims, and Allowed Priority Non-Tax Claims, (ii) funding of the Wind Down Reserve with the Wind Down Amount ($3,000,000) in accordance with the Wind Down Budget, (iii) funding of the

First Lien Reserve, (iv) funding of the GUC Reserve, and (v) funding of the Professional Fee Escrow Account and payment of Professional Fee Claims therefrom. In addition to the Professional Fee Escrow Account, the Liquidation Trustee will

establish a separate account for each of the Senior Claims Reserve, Wind Down Reserve, GUC Reserve, First Lien Reserve, and Second Lien Reserve, each to be maintained by the Liquidation Trustee in accordance with the Plan.

The Liquidation Trustee shall make Plan Distributions, as applicable, in the frequency determined in the Liquidation Trustee’s discretion, in accordance with the Plan:

Holders of Other Secured Claims will either receive (i) payment in full in Cash of their Allowed Claims, (ii) other treatment to render them unimpaired, or (iii) such other recovery to satisfy

section 1129 of the Bankruptcy Code.

11

Holders of First Lien Noteholder Secured Claims will receive their pro rata share of First Lien Liquidation Trust Interests, which beneficial interests will entitle them to the Excess Cash to be

allocated pursuant to the Waterfall, until they receive the allowed amount of their Claims.

Holders of Second Lien Noteholder Secured Claims will receive their pro rata share of Second Lien Liquidation Trust Interests, which beneficial interests will entitle them to the Excess Cash

remaining after all First Lien Noteholder Secured Claims are satisfied in full pursuant to the Waterfall.

Holders of General Unsecured Claims, including any deficiency claims of the First Lien Noteholders and the Second Lien Noteholders, as well as the claims of the Unsecured Noteholders, will receive

their pro rata share of the GUC Liquidation Trust Interests, which beneficial interests will entitle them to share in a GUC Reserve that consists of (i) the GUC Residual Amount,1 if any, (ii) the GUC Reserve Funding Amount of $1,500,000.00, (iii) the Retained Causes of Action belonging to each of the Debtors and the Debtors’ Estates and the proceeds thereof (including any D&O Policy proceeds payable

to the Estate on account of settlements or judgments from Commercial Tort Claims and other non-released claims and Causes of Action), and (iv) the Unencumbered Assets, and (v) the proceeds of each of the foregoing clauses (i)-(iv), which in the case of clauses (ii), (iii), and (iv) shall be transferred to the Liquidation Trust on the Effective Date, and in the case of clauses (i) and (v) shall be transferred to the Liquidation Trust on the Effective Date

or as soon as reasonably practicable thereafter in accordance with the Plan, free and clear of all Claims, Liens, and encumbrances.

For purposes of making distributions under the Plan to Holders of General Unsecured Claims, the Debtors’ assets and liabilities will be substantively consolidated, and as such, treated as if they

belonged to a single combined entity. As a result, a General Unsecured Claim against any one Debtor will be treated as a single General Unsecured Claim against the combined Debtors, rather than as separate claims against each individual Debtor.

After the Effective Date, pursuant to the Plan, the Liquidation Trustee shall, in an expeditious but orderly manner, wind down, sell, and otherwise liquidate and convert to Cash the

remaining assets of the Debtors, with no objective to continue or conduct a trade or business except to the extent reasonably necessary to, and consistent with, the liquidation and orderly wind down of the Debtors and shall not unduly prolong the

duration of the liquidation and the wind down.

To the extent the Liquidation Trustee generates Excess Cash after the Effective Date from monetizing the Liquidation Trust Assets, including the receipt of any Surplus Reserved

Cash, Surplus Senior Claims Reserve Cash, and Surplus Professional Fee Escrow Account, such proceeds shall be allocated pursuant to the Waterfall as set forth below.

For cash remaining after the initial funding of reserves on the Effective Date, derived from the monetization of non-GUC Reserve Assets of the Liquidation Trust, or received from

surplus reserve amounts, such proceeds shall be distributed through the Waterfall in the following order:

| 1. |

to fund any deficits in the Senior Claims Reserve;

|

| 2. |

to fund the First Lien Reserve for the benefit of First Lien Noteholders;

|

| 1 |

The “GUC Residual Amount” means any Excess Cash remaining after (i) any deficits in the Senior Claims Reserve are satisfied in accordance with the Plan, (ii) Holders of First Lien Liquidation Trust Interests receive an amount equal to

their Allowed First Lien Noteholder Secured Claims, and (iii) Holders of Second Lien Liquidation Trust Interests receive an amount equal to their Allowed Second Lien Noteholder Secured Claims.

|

12

| 3. |

to fund the Second Lien Reserve for the benefit of Second Lien Noteholders; and

|

| 4. |

as the GUC Residual Amount, if any, to be distributed to Holders of General Unsecured Claims.

|

For cash (i) derived from the monetization of GUC Reserve Assets of the Liquidation Trust or (ii) remaining as GUC Residual Amount, such proceeds shall be

applied in the following order:

| 1. |

to fund up to $200,000.00 of the Creditors’ Committee Fees in excess of the Creditors’ Committee Fee Cap;

|

| 2. |

to fund the GUC Reserve for the benefit of Holders of General Unsecured Claims.

|

Furthermore, the Office of Foreign Assets Control (“OFAC”) has issued a blocking order for 5% of Luminar Parent shares (the “Blocked

Parent Interests”). As a result, pursuant to OFAC regulations, the Debtors are prohibited from dealing in, or otherwise affecting, the Blocked Parent Interests prior to obtaining an OFAC License. The Debtors are preparing to apply for

such an OFAC License, but the timing of obtaining such license is to be determined. Therefore, the Debtors’ Plan provides that on the Effective Date, to the extent the Debtors have not secured an OFAC License, (i) all Parent Interests, other than

the Blocked Parent Interests, will be cancelled and (ii) substantially contemporaneously, new common stock in the Parent Debtor of the same number, class, and series as the Unblocked Parent Interests that are cancelled pursuant to section 4.9 of

the Plan will be issued to the Liquidation Trust. The Parent Debtor Additional Stock shall be held only (and not transferred by) the Liquidation Trust and, once the Debtors have secured the OFAC License and can cancel the Blocked Parent Interests,

the Liquidation Trust will be entitled to subsequently cancel all remaining Interests (including the Blocked Parent Interests) and wind down Luminar Technologies, Inc.

Any right to receive a Distribution from the Liquidation Trust will not, and is not intended to, constitute “securities” and, accordingly, will not be

registered pursuant to the Securities Act or any applicable state or local securities law. However, if it should be determined that any such right to receive such Distributions constitute “securities,” the exemption provisions of section 1145 of

the Bankruptcy Code will be satisfied and the offer and sale under the Plan of such right will be exempt from registration under the Securities Act, all rules and regulations promulgated thereunder, and all applicable state and local securities

laws and regulations. Any such right to receive such Distributions (and the underlying Claim giving rise thereto) shall not: (a) be voluntarily or involuntarily, directly or indirectly, assigned, conveyed, hypothecated, pledged, or otherwise

transferred or traded; (b) be evidenced by a certificate or other instrument; and (c) possess any voting rights with respect to the Liquidation Trust or otherwise, except as otherwise provided in the governing documents thereof.

The Debtors believe the Plan maximizes value for all stakeholders.

| B. |

GLOBAL SETTLEMENT

|

The Debtors, the Ad Hoc Noteholder Group, and the Creditors’ Committee have engaged in good faith and arm’s length negotiations, culminating in the parties’ entry into the Global Settlement. The

Global Settlement is incorporated into the Plan and provides for the resolution of all disputes, claims, and controversies between the parties, including those related to the Plan and treatment of general unsecured claims, among other issues.

The Global Settlement includes, among others, the following material terms and conditions (each as set forth in the Plan):

13

| • |

Holders of General Unsecured Claims (including First Lien Noteholder Deficiency Claims, if any, and Second Lien Noteholder Deficiency Claims) shall receive GUC Liquidation Trust Interests entitling them to their Pro Rata Share of Cash

consisting of the GUC Reserve Assets and any proceeds thereof, net of any costs and expenses incurred by the Liquidation Trust (including fees of the Liquidation Trustee and any taxes incurred by the Liquidation Trustee, whether such taxes

are incurred directly by the Liquidation Trustee in his or her role as such, or on account of those taxes attributed proportionately to each Holders’ share of GUC Liquidation Trust Interests) in connection with the pursuit, abandonment, or

liquidation of all GUC Reserve Assets;

|

| • |

GUC Reserve Assets shall include (i) the GUC Residual Amount, if any, (ii) the GUC Reserve Funding Amount of $1,500,000.00, (iii) the Retained Causes of Action belonging to each of the Debtors and the Debtors’ Estates and the proceeds

thereof (including any D&O Policy proceeds payable to the Estate on account of settlements or judgments from Commercial Tort Claims and other non-released claims and Causes of Action), and (iv) the Unencumbered Assets, and (v) the

proceeds of each of the foregoing clauses (i)-(iv);

|

| • |

The appointment of the Liquidation Trustee shall be mutually agreeable between the Ad Hoc Noteholder Group and the Creditors’ Committee and reasonably acceptable to the Debtors; the Creditors’ Committee shall select each of the three

members of the Liquidation Trust Oversight Board;

|

| • |

The Debtors shall be deemed substantively consolidated for purposes of distributions to Holders of General Unsecured Claims;

|

| • |

All Preference Actions against the Debtors’ trade vendors shall be deemed released on the Effective Date;

|

| • |

The Ad Hoc Noteholder Group consents to permit the Debtors to use Cash Collateral through the Effective Date;

|

| • |

The sum of the Allowed Professional Fee Claims of the Creditors’ Committee Advisors and the Restructuring Fees and Expenses due to the Unsecured Notes Trustee shall be capped at $4.225 million; provided

that any amounts up to $200,000 incurred in excess of $4.025 million shall be payable from the first dollars to be distributed as Post Effective Date Available Cash (GUC Reserve Assets); and

|

| • |

Only if the Effective Date of the Plan occurs on or before April 14, 2026, the aggregate Allowed Professional Fee Claims of the Debtors’ Advisors (excluding any amounts paid pursuant to the Ordinary Course Professionals Retention Order)

shall not exceed $26.471 million.

|

The Debtors, the Ad Hoc Noteholder Group, and the Creditors’ Committee believe that the Global Settlement avoids potentially costly, time-consuming, and wasteful litigation and any related delays

in distributions to creditors. The Debtors, the Ad Hoc Noteholder Group, and the Creditors’ Committee likewise believe the Global Settlement balances the desires of the key constituents in these cases and provides an equitable solution that is

reasonable, fair and efficient. For these and other reasons described above, the Creditors’ Committee recommends that creditors in class 5 vote to ACCEPT the Plan.

14

| C. |

TREATMENT OF CLAIMS AND INTERESTS

|

The following table summarizes (i) the type of Claims and Interests under the Plan, (ii) which Classes are impaired by the Plan, and (iii) which Classes are entitled to vote on the Plan. The table

is qualified in its entirety by reference to the full text of the Plan.

| 1. |

Claims and Interests in Luminar Technologies, Inc.

|

|

Designation

|

Total Est. Claims3

|

||||||

|

Class 1: Other Priority Claims

|

Except to the extent that a Holder of an Allowed Other Priority Claim agrees to a less favorable treatment of such Claim, each such Holder shall receive, in full and final satisfaction, settlement, release,

and discharge of such Claim, on or as soon as reasonably practicable after the later of the Effective Date and the date that is thirty (30) calendar days after the date such Other Priority Claim becomes an Allowed Claim, at the option of

the Debtors or Liquidation Trustee (as applicable), either (i) payment in full in Cash or (ii) other treatment consistent with the provisions of section 1129(a)(9) of the Bankruptcy Code.

|

Unimpaired

|

No (Presumed to Accept)

|

$0.8M

|

100%

|

||

|

Class 2: Other Secured Claims

|

Except to the extent that a Holder of an Allowed Other Secured Claim agrees to less favorable treatment of such Claim, each Holder of an Allowed Other Secured Claim shall receive, at the option of the Debtors

or the Liquidation Trustee, as applicable, in full and final satisfaction, settlement, release, and discharge of such Claim, on the Effective Date or as soon as reasonably practicable thereafter: (i) payment in full in Cash in an amount

equal to the Allowed amount of such Other Secured Claim; (ii) such other treatment sufficient to render such Holder’s Allowed Other Secured Claim Unimpaired pursuant to section 1124 of the Bankruptcy Code; or (iii such other recovery

necessary to satisfy section 1129 of the Bankruptcy Code.

|

Unimpaired

|

No

|

$8.0M

|

100%

|

|

2

|

Nothing in the Plan or Confirmation Order shall grant the Debtors a discharge pursuant to section 1141(d) of the Bankruptcy Code.

|

|

3

|

The total estimated claim amounts are based on preliminary claims estimates and are subject to material change, including on account of any additional claims that may be Filed and Allowed, such as rejection

damages claims. Additional information regarding the assumptions and qualifications regarding this recovery table is set forth in Section I.C.2.

|

15

|

Class

Designation

|

Plan Treatment2 | Impairment | Entitlement to Vote | Total Est. Claims3 | Approx. Percentage Recovery | ||

|

Class 3: First Lien Noteholder Secured Claims

|

Except to the extent that a Holder of a First Lien Noteholder Secured Claim agrees to a less favorable treatment of such Claim, each such Holder shall receive, in full and final satisfaction, settlement,

release, and discharge of such Claim, on the Effective Date or as soon as reasonably practicable thereafter, such Holder’s Pro Rata Share of the First Lien Liquidation Trust Interests.

|

Impaired

|

Yes

|

$24.0M

|

100%

|

||

|

Class 4: Second Lien Noteholder Secured Claims

|

Except to the extent that a Holder of a Second Lien Noteholder Secured Claim agrees to a less favorable treatment of such Claim, each such Holder shall receive, in full and final satisfaction, settlement,

release, and discharge of such Claim, on the Effective Date or as soon as reasonably practicable thereafter, such Holder’s Pro Rata Share of the Second Lien Liquidation Trust Interests.

|

Impaired

|

Yes

|

$14.0M

|

48–100%

|

||

|

Class 5: General Unsecured Claims

|

Except to the extent that a Holder of an Allowed General Unsecured Claim agrees to a less favorable treatment of such Claim, each such Holder shall receive, in full and final satisfaction, settlement,

release, and discharge of such Claim, on the Effective Date or as soon as reasonably practicable thereafter, such Holder’s Pro Rata Share of the GUC Liquidation Trust Interests.

|

Impaired

|

Yes

|

$518.8M

|

0–1%

|

||

|

Class 6: Intercompany Claims

|

On or before the Effective Date or as soon as reasonably practicable thereafter, all Intercompany Claims shall be adjusted, Reinstated, or discharged (each without any distribution) to the extent reasonably

determined to be appropriate by the Debtors or Liquidation Trustee (as applicable).

|

Impaired

|

No (Deemed to Reject)

|

$6.8M

|

None.

|

||

|

Class 7: Intercompany Interests

|

On the Effective Date, and without the need for any further corporate or limited liability company action or approval of any member, board of directors, board of managers, managers, management, or Security

Holders of any Debtor, all Intercompany Interests shall be cancelled, released, and extinguished, by distribution, contribution or otherwise, as determined by the Debtors or the Liquidation Trustee (as applicable); provided that no Plan Distributions shall be made to Holders of an Intercompany Interest on account of such Intercompany Interest under the Plan.

|

Unimpaired / Impaired

|

No (Deemed to Reject)

|

N/A

|

None.

|

16

|

Class

Designation

|

Plan Treatment2 | Impairment | Entitlement to Vote | Total Est. Claims3 | Approx. Percentage Recovery | ||

|

Class 8: Subordinated Claims

|

All Subordinated Claims, if any, shall be discharged, cancelled, released, and extinguished as of the Effective Date, and will be of no further force or effect, and Holders of Allowed Subordinated Claims will

not receive any distribution on account of such Claims.

|

Impaired

|

No (Deemed to Reject)

|

N/A

|

None.

|

||

|

Class 9: Parent Interests

|

Without the need for any further corporate or limited liability company action or approval of any board of directors, management, or Security Holders of any Debtor, as applicable, all Parent Interests shall

be cancelled (i) on the Effective Date, with respect to all Unblocked Parent Interests and (ii) after OFAC issues the OFAC License, with respect to all Blocked Parent Interests, and the Holders of Parent Interests will not receive or retain

any property on account of such Parent Interests under the Plan.

|

Impaired

|

No (Deemed to Reject)

|

N/A

|

None.

|

| 2. |

Key Recovery Table Assumptions and Qualifications

|

The recovery table above estimates ~$32.2 to $39.4 million of net proceeds are available for recovery to creditors, after the Asset Sale Offer (as defined and described below), and the funding of

the Wind Down Trust ($3.0 million) and Liquidation Trust, and include (i) estimated cash and cash equivalents based on the Approved Budget under the Final Cash Collateral Order and includes estimated proceeds from the LiDAR Sale Transaction, (ii)

estimated recoveries on accounts receivables, (iii) a 50–100% recovery of the $11.0 million LSI Post Closing Indemnity Escrow; and (iv) other assets and PP&E, including estimated recoveries on the NEXT Note and SAFE Note, proceeds from the sale

of real property in Florida, and any remaining value distributed from or liquidated at the international or other non-debtor subsidiaries.

The calculations in the recovery table assume (i) that $89.35 million of proceeds from the LSI Sale Transaction are used to redeem at least 80% of the First Lien

Noteholders Secured Claims at 103% plus accrued interest on or about March 11, 2026 pursuant to an Asset Sale Offer made in accordance with section 3.12 of, and as defined in, the 1L Notes Indenture (as defined below) (ii) the remaining First Lien

Noteholder Secured Claims (estimated at $24.0 million) are paid in full pursuant to the distributions made pursuant to the Plan at a redemption price of 111% plus accrued interest through the payment date. Additional information regarding the

Asset Sale Offer is set forth in Section IV.G.3. hereof.

17

Based on the estimated proceeds available for distribution and estimated participation in the Asset Sale Offer, the Debtors have estimated the Second Lien Noteholder Secured Claims at

$14.0 million, which amount is the highest expected recovery for such Holders after the First Lien Noteholder Secured Claims are satisfied under the Plan. The estimated unpaid portion of the Second Lien Noteholder Claim Amount4 after payment on account of the Second Lien Noteholder Secured Claims is approximately $259 million, which is considered a Second Lien Deficiency Claim under the Plan

and classified as General Unsecured Claims.

The Debtors have estimated approximately $519 million of General Unsecured Claims consisting of estimated Second Lien Deficiency Claims (~50%), Unsecured Notes (26%), and estimated trade accounts

payable and potential rejection damages (~24%).

| D. |

VOTING PROCEDURES

|

For each holder of a Claim or Interest entitled to vote on the Plan, the Debtors will provide each party with, among other things, a copy of the Disclosure Statement, the Plan, a Ballot, and voting

instructions regarding how to properly complete the Ballot and submit a vote with respect to the Plan. For detailed voting instructions, please refer to the voting instructions and the Ballot enclosed with this Disclosure Statement.

All completed Ballots must be actually received by Omni Agent Solutions, Inc. (“Omni”), the Debtors’ claims, noticing, and balloting agent (the “Voting Agent”), at the below address no later than the Voting Deadline.

If you are holder of a Claim or Interest that is entitled to vote on the Plan and you did not receive a Ballot, received a damaged Ballot, or lost your Ballot, or if you have any questions

concerning the Disclosure Statement, the Plan, or the procedures for voting with respect to the Plan, please contact Omni at (888) 901-3403 (for holders of Claims or Interests in the U.S. and Canada; toll-free) or +1 (747) 293-0190 (for holders of

Claims or Interests located outside of the U.S. and Canada) or via e-mail message (with “Luminar Solicitation” in the subject line) to LuminarInquiries@OmniAgnt.com.

Sections 11.3, 11.4, 11.5, 11.6, 11.7, 11.8 and 11.9 of the Plan also contain certain release, injunction, and exculpation provisions, each of which are reproduced on Exhibit D hereto. If you hold a Claim or Interest and do not timely, properly, and affirmatively elect to opt-out of the releases contained in Section 11.6(b) of the Plan, then you shall be deemed to consent to the releases

contained in Section 11.6(b) and elect to release claims against the “Released Parties”.

| 4 |

“Second Lien Noteholder Claim Amount” means, for each Second Lien Noteholder, the remaining outstanding principal owed, after taking into account any payments made pursuant to an Asset Sale Offer (as defined in the Second Lien Notes

Indenture) before the Effective Date in accordance with section 3.12 of the Second Lien Notes Indenture, plus, without duplication, any interest (including, if applicable, Default Interest (as defined in the Second Lien Notes Indenture),

unpaid fees, expenses, and indemnities of the Second Lien Notes Agent, in each case accrued and unpaid through the Petition Date, to the extent provided under the Second Lien Notes Indenture and the Bankruptcy Code, plus 50% of the

Make-Whole Premium (as defined in the Second Lien Notes Indenture) that would have otherwise been included in the calculation of the Redemption Price (as defined in the Second Lien Notes Indenture) of the Second Lien Notes. For the

avoidance of doubt, the Second Lien Noteholder Claim Amount shall be calculated based on the remaining balance outstanding on the Second Lien Noteholder Claims following any payments made pursuant to an Asset Sale Offer.

|

18

|

THE VOTING AGENT WILL NOT COUNT ANY BALLOTS RECEIVED AFTER THE VOTING DEADLINE, UNLESS THE DEBTORS, SHALL HAVE GRANTED AN EXTENSION OF THE VOTING DEADLINE IN WRITING WITH RESPECT TO SUCH BALLOT OR WAIVE THE

LATE SUBMISSION.

|

| A. |

COMPANY’S BACKGROUND AND FORMATION

|

Headquartered in Orlando, Florida, the Debtors are a technology company specializing in advanced Light Detection and Ranging (“LiDAR”) hardware and software

solutions to enable the world’s safest and smartest vehicles. In the last decade, the Company has been developing proprietary LiDAR hardware, core semiconductor components, and software – in-house – to meet the demanding performance, safety,

reliability and cost requirements to enable next-generation safety and autonomous (self-driving) capabilities for passenger and commercial vehicles, as well as other adjacent markets.

Austin Russell founded the Company on December 12, 2012, with the goal of developing preeminent LiDAR technology that could be used in passenger and commercial vehicles (including to facilitate the

autonomous operation of cars, trucks, and robotaxis), among other applications, and ultimately save lives by significantly reducing vehicle collisions. As described below in more detail, LiDAR technology is the most advanced sensor technology

available for autonomous driving and significantly improves safety functions in vehicles by providing increased situational awareness in a broad range of driving environments through improved and higher confidence detection and planning at all

vehicle speeds. Yet, prior to the Company’s founding, LiDAR technology was primarily used in defense and aerospace applications and was virtually absent from the civilian automotive market. Given the complexities attendant to integrating LiDAR

technology into the multifaceted automotive systems embedded in autonomous cars, no company had successfully integrated LiDAR into consumer vehicles at the time the Company was founded.

The Company distinguished itself in the industry by (i) focusing its business primarily on applying LiDAR technology in the automotive industry through partnerships with major original equipment

manufacturers (“OEMs”) (as opposed to other smaller, at the time, markets like robotics and drones), (ii) using a higher wavelength laser, which provides superior performance, and (iii) building its LiDAR

technology in-house (as opposed to a product composed of unaffiliated off-the-shelf parts), facilitated through a series of strategic acquisitions. In so doing, the Company offered its customers best-in-class LiDAR systems. These efforts required

significant investment to develop groundbreaking LiDAR technology while simultaneously integrating multiple businesses and their associated products into the Company’s business model.

In its first few years, the Company generally operated out of the public eye to protect its intellectual property and develop its business. Over time, the Company made several acquisitions,

entered into multiple partnerships to grow its business while continuing to develop its technology, and went public to raise more capital for these initiatives.

19

BFE Acquisition. The Company’s first strategic acquisition was its 2018 acquisition of BFE Acquisition Sub II, LLC d/b/a Black Forest Engineering (“BFE”),

a provider of advanced photonic hardware and firmware solutions. This transaction was the Company’s initial step in executing on its growth strategy of being able to develop the chip technology necessary to build LiDAR units wholly in-house and

scale its business to meet growing customer demand.

LSI Acquisitions. In August 2021, the Company acquired OptoGration, Inc. (“OptoGration”), a manufacturer of photodetectors (i.e., electronic devices that convert light into an electrical signal, such as a current or voltage), including photodiodes, quadrant detectors, focal plane arrays, and short-wave infrared single-photon avalanche diodes. In April

2022, the Company acquired Freedom Photonics LLC (“Freedom Photonics”), a designer and manufacturer of high-performance lasers and related photonic products exclusively for external customers. In 2023, the

Company began to refer to OptoGration and Freedom Photonics as the LSI side of the business, or LSICo. On March 18, 2024, the Company further augmented LSICo by acquiring EM4, LLC (“EM4”), a designer,

manufacturer, and seller of packaged photonic components and sub-systems for aerospace and industrial markets.

Public Listing. In December 2020, the Company went public in a de-SPAC transaction, and its Class A common stock of the Company began trading on the Nasdaq Global Select Market under the

ticker symbol “LAZR”.5 The de-SPAC transaction enabled the Company to raise over $500 million cash.

Key Partnerships. The Company entered into several key partnerships over the years, as described below:

| • |

Volvo Partnership. In March 2020, the Company signed the automotive industry’s first deal for LiDAR production for autonomous consumer vehicles through a contract with Volvo. At the time

of the agreement, Volvo was expected to make the Company’s LiDAR technology part of the standard safety package on its next generation electric SUV, the EX90. After several years of development under the contract, Volvo required the

Company to demonstrate that it could make enough LiDAR components to represent a full year’s production. To meet these demands, the Company continued to expand and invest in its business and demonstrated it could produce the required

100,000+ LiDAR components in 2024. This investment did not yield the intended results, as Volvo only purchased less than 10,000 LiDAR components over the next eighteen (18) months.

|

| • |

Polestar Partnership. In September 2021, Polestar Automotive Holding UK PLC (“Polestar”) disclosed that it would integrate the Company’s technology

into certain of its future production vehicles. In October 2022, Polestar unveiled the Polestar 3 electric performance SUV and announced that Luminar LiDAR would be an optional feature available for customers in the second quarter of

2023. However, after repeated project delays, Polestar discontinued the offering because the vehicle’s software ultimately could not use the LiDAR features, and the contract terminated.

|

| 5 |

Specifically, the Company’s predecessor, Gores Metropoulos, Inc. (“Gores Metropoulos”), a special purpose acquisition company, and Dawn Merger Sub, Inc. (“Merger

Sub I”) and Dawn Merger Sub II, LLC (“Merger Sub II”), each a wholly-owned direct subsidiary of Gores Metropoulos, consummated a merger with pre business-consummation Luminar Technologies, Inc. (“Legacy Luminar” and, such transaction the “Merger”) whereby Gores Metropoulos, Merger Sub I, and Merger Sub II

merged with and into Legacy Luminar, with Gores Metropoulos being the surviving corporation. Upon the closing of the Merger, Gores Metropoulos changed its name to Luminar Technologies, Inc.

|

20

| • |

Mercedes Partnership. In January 2022, the Company announced a partnership with Mercedes-Benz (“Mercedes”) to accelerate the development of future

automated driving technologies for Mercedes passenger cars. In the first quarter of 2023, Mercedes indicated it planned to integrate the Company’s LiDAR across a broad range of its next-generation production vehicle lines, as optional

equipment, by mid-decade. However, after the Company failed to meet ambitious requirements, Mercedes terminated the development and supply agreement for breach in November of 2024. The Company and Mercedes entered into a non-exclusive

development agreement for Halo in March of 2025, however, at this time, the Company has no go-forward projects with Mercedes.

|

| B. |

BUSINESS OPERATIONS

|

The Company operated two distinct, but interconnected, business segments, each under a separate vertical of the Company’s organizational structure: (i) autonomy solutions, which is housed at

Luminar Parent, Luminar, LLC, and certain of their subsidiaries (collectively, “LiDARCo”); and (ii) advanced technologies and services (“ATS”), which is housed in

LSICo. Together, LiDARCo and LSICo developed proprietary LiDAR hardware, core semiconductor components, and software to meet demanding performance, safety, reliability, and cost requirements to enable next-generation safety and autonomous

capabilities for passenger and commercial vehicles and other adjacent markets. The LSICo entities are not Debtors in these chapter 11 cases. Instead, as described below, the Debtors prosecuted these cases, in part, to sell their equity interests

in LSICo pursuant to section 363 of the Bankruptcy Code.

| 1. |

LiDARCo

|

Luminar Parent oversees the Company’s LiDARCo autonomy solutions business and, together with certain of its subsidiaries, houses, develops, and markets the Company’s LiDAR sensors. Specifically,

LiDARCo manufactures and sells LiDAR sensors, with a focus on OEMs in the automotive industry, robotaxis, and adjacent industries. Additional supporting functions within this segment include (i) non-recurring engineering (“NRE”) services related to the Company’s LiDAR products, (ii) the development of related software products, packaged as SentinelTM (an autonomous driving and safety software, which combines the Company’s LiDAR,

perception software, and HD mapping), and (iii) the licensing of certain data and information.

The Company pioneered the use of LiDAR technology in vehicles. It was the first company to build a LiDAR sensor for use in the roofline of vehicles—a practice that has now become the global

standard. Moreover, the Company’s LiDAR technology enables higher speed highway autonomy as compared to its competitors because it operates with a higher wavelength laser that detects critical objects further away. The Company’s LiDAR sensors

measure distance using pulsed laser light to generate a 3D model of the surrounding environment. Unlike cameras and radar, the Company’s LiDAR sensors provide precise, three-dimensional sight in all lighting conditions, even in blinding light or

of dark objects at night up to 300 meters away.

The first LiDAR model the Company successfully brought to the consumer vehicle market, Iris LiDAR (“Iris”), is a high performance, long-range sensor, built

from the chip-up, that unlocks safety and autonomy for vehicles. Iris and its variants feature the Company’s vertically integrated receiver, detector, and application-specific integrated circuit (ASIC) solutions developed by LSICo. The Company

announced Iris’s launch shortly after partnering with Volvo in 2020, and it achieved start of production (“SOP”) in April 2024.

21

Luminar Halo (“Halo”), which the Company unveiled in 2024, is the Company’s next-generation and most technologically-advanced model of LiDAR technology.

Halo is designed to combine unmatched performance in a pocket-sized package for high-volume production vehicles. Halo offers step-function improvements in performance, integration, and cost, as compared to Iris. Despite its smaller size, Halo can

see faster, farther, and more precisely than any of today’s LiDAR solutions, and its advancements are expected to enable a 2x improvement in performance, a 3x reduction in size, and a more than 2x improvement in cost. The Company is currently

targeting SOP of Halo by 2027.

A key differentiator of the Company’s LiDAR technology, as compared to its competitors, is its use of a 1550nm laser, as opposed to the 905nm laser. The 1550nm laser allows for the detection of

objects from longer distances, at higher speeds, and in more challenging conditions compared to the 905nm laser. In addition, the Company’s technology is the only LiDAR product on the market that (i) meets OEM specifications to enable highway

autonomy for consumer series production and (ii) was made standard on a global production vehicle (the Volvo EX90).

| 2. |

LSICo

|

LSI and its subsidiaries oversee the Company’s ATS businesses, developing components that can be used in the Company’s LiDAR sensors, as well as other applications. Specifically, LSICo is a

vertically integrated photonics company that supplies critical components, subsystems (including semiconductor lasers and photodetectors), and systems to Luminar and third parties. The operations of OptoGration, Freedom Photonics, and EM4 fall

within the LSICo segment and together provide advanced hardware and custom developed components to power the Company’s LiDAR technology, as well as design, testing, and consulting services to LiDARCo and third-party customers. In particular,

OptoGration is a critical supplier to LiDARCo as well as to external customers in other industries, including energy, military, and space.

Photonics is the science and technology of generating, manipulating, and detecting photons (or light). LSICo offers the full vertical stack of photonics solutions enabling the Company to utilize

its own supply chain to build best-in-class LiDAR technology. LSICo’s products and capabilities (which span photon generation, interaction, and detection) are also applicable to a wide range of rapidly growing industries, including aerospace and

defense, quantum sensing and networking, and telecommunications. Third parties to which LSICo’s diverse range of photonics solutions are deployed include government agencies and contractors in a range of applications, including missile defense,

quantum sensing and networking, directed energy, and autonomous systems, among others.

LSICo operates four (4) facilities across the United States: Boston, Massachusetts (two (2) facilities); Princeton, New Jersey; and Santa Barbara, California. In those facilities, LSICo performs

end-to-end capabilities from wafer fabrication to subsystem integration; in-house research and development and low-volume wafer production; space-grade and other advanced packaging functions; optical component qualification and reliability testing;

and design and assembly functions for their subsystems; optical component qualification and reliability testing; and design and assembly of complex micro-optic subsystems.

Because LSICo’s capabilities span photon generation, interaction, and detection, LSICo provides a unified photonics architecture, delivering full-stack photonics solutions for defense and

enterprise applications. In addition, LSICo’s advanced packaging expertise allows it to produce integrated systems that meet U.S. Department of Defense and enterprise specifications. Moreover, LSICo’s photonics solutions address significant

capability gaps critical to technologies of the Department of Defense. LSI is a secure 100% domestic supplier for national security purposes.

22

| C. |

CORPORATE STRUCTURE AND GOVERNANCE

|

| 1. |

Corporate Structure

|

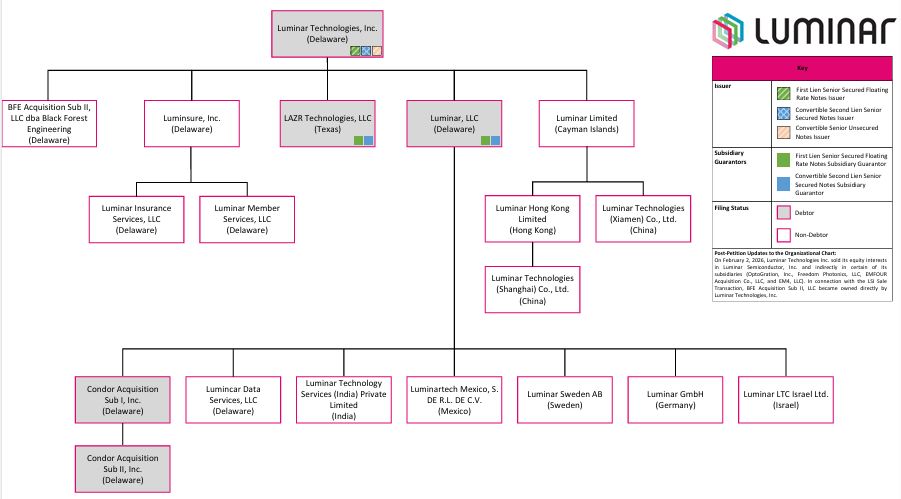

A chart summarizing the Debtors’ corporate organization structure, as of the date hereof, is annexed hereto as Exhibit B. The Company consists of nineteen (19) legal entities organized in multiple jurisdictions, of which five (5) are Debtors. Luminar Parent directly or indirectly owns the other Debtors.6

On May 14, 2025, following a code of business conduct and ethics inquiry by the Board’s audit committee, Mr. Russell, who had been the Company’s Chief Executive Officer (“CEO”) since its founding, resigned as the Company’s President and CEO and as Chairperson of the Board. That day, the Board appointed Paul Ricci as the Company’s CEO, effective on or about May 21, 2025, and to the Board. The

Company chose Mr. Ricci, a seasoned executive with decades of experience leading technology companies, to help navigate institutional challenges and guide the business in a positive direction.

On October 31, 2025, the Company announced that Thomas J. Fennimore would step down as the Company’s Chief Financial Officer (the “CFO”), effective November

13, 2025, to pursue other career opportunities. On November 7, 2025, the Company appointed Thomas Beaudoin as its CFO, effective November 13, 2025.

As of the Petition Date, Luminar Parent’s board of directors (the “Board”) consisted of eleven (11) directors: Elizabeth Abrams, Patricia Ferrari, Alec E.

Gores, Dr. Mary Lou Jepsen, Dr. Shaun Maguire, Katharine A. Martin, Paul Ricci, Austin Russell, Dominick Schiano, Matthew J. Simoncini, and Daniel D. Tempesta. Ms. Abrams and Ms. Ferrari, who both have substantial restructuring experience, were

appointed to the Board as independent directors on November 12, 2025.

The Company’s senior management team consists of the following individuals: Paul Ricci, Thomas Beaudoin, and Alexander Fishkin.

On November 12, 2025, the Board established a special investigation committee comprised of Ms. Abrams and Ms. Ferrari (the “Special

Investigation Committee” or “SIC”). The Special Investigation Committee is authorized to, among other things, review, evaluate, pursue, negotiate, approve, and authorize any disposition of any

potential claims or causes of action against any of the Board’s current, former, or future director, officer, insider, affiliate, or other related party. Before the Petition Date, the SIC retained King & Spalding LLP (“K&S”) to assist the SIC and Weil with an investigation of certain acts, omissions, transactions and potential claims and causes of action involving or related to

certain current and former directors and officers of Luminar Technologies, Inc. and its affiliates.

| 6 |

On February 2, 2026, Luminar Technologies, Inc. sold its equity interests in Luminar Semiconductor, Inc. and indirectly in certain of its subsidiaries (OptoGration, Inc., Freedom Photonics, LLC, EMFOUR Acquisition Co., LLC, and EM4,

LLC). In connection with the LSI Sale Transaction, BFE Acquisition Sub II, LLC became owned directly by Luminar Technologies, Inc.

|

23

On November 24, 2025, the Board (i) renamed a pre-existing special committee7 the Special Transactions Committee (“STC”), (ii) changed the composition of the STC, including to add Ms. Abrams and Ms. Ferrari, and (iii) updated the STC’s mandate. The STC is authorized to, among other things, evaluate potential transactions

that may involve Luminar Parent and one or more of its subsidiaries, on the one hand, and Mr. Russell, on the other hand (each, a “Covered Transaction”), recommend that the Board authorize the Company to

enter into a Covered Transaction, oversee Company management and its advisors with respect to discussions and negotiations concerning a Covered Transaction, and oversee the implementation and execution of a Covered Transaction. On December 8, 2025, the Board further expanded the STC’s mandate to include the evaluation of and ability to make a recommendation on certain other transactions. The current members of the STC are Ms. Abrams, Ms.

Ferrari, Dr. Jepsen, Ms. Martin, Mr. Simoncini, and Mr. Tempesta.

| 2. |

Capital Structure

|

As of the Petition Date, the Debtors had approximately $488 million in funded debt obligations comprised of the Company’s obligations under the (i) 1L Notes Indenture (as defined below), (ii) 2L

Notes Indenture (as defined below), and (iii) Unsecured Notes Indenture (as defined below). A summary of the Debtors’ outstanding funded debt obligations as of the Petition Date is set forth below:

|

Approximate Amount Outstanding as of Petition Date(1)

|

|

|

Secured Funded Debt

|

|

|

Floating Rate Senior Secured Notes due 2028

|

$104.4 million

|

|

9.0% Convertible Second Lien Senior Secured Notes due 2030

|

$57.3 million

|

|

11.5% Convertible Second Lien Senior Secured Notes due 2030

|

$189.7 million

|

|

Unsecured Funded Debt

|

|

|

1.25% Convertible Senior Notes due 2026

|

$135.7 million

|

|

Total Funded Debt

|

$487.1 million

|

|

(1) Includes estimated accrued interest through December 15, 2025.

|

|

| a. |

First Lien Notes

|

On August 8, 2024, certain of the Debtors entered into that certain first lien indenture (the “1L Notes Indenture”), by and among Luminar, as issuer, certain

subsidiaries of the Company, as guarantors (in such capacity, the “Notes Guarantors”), and GLAS Trust Company LLC, as trustee and collateral agent (in such capacity, the “1L

Collateral Agent”), pursuant to which the Company issued $100.0 million in aggregate principal amount of Floating Rate Senior Secured Notes due 2028 (the “1L Notes”). The 1L Notes bear interest at a

floating rate equal to Term secured overnight financing rate (“SOFR”) plus 9.0%, subject to a Term SOFR floor of 3.0%, resulting in an effective interest rate of 14.8% as of September 30, 2025. Interest is

payable quarterly in arrears on February 15, May 15, August 15, and November 15 of each year. The 1L Notes mature on the earlier of (i) August 15, 2028 or (ii) September 15, 2026 if, as of June 30, 2026, more than $100.0 million of Unsecured

Convertible Notes remain outstanding. As of the Petition Date, the aggregate principal amount of 1L Notes outstanding was approximately $104.4 million including accrued and unpaid interest. As described in Section IV.G.3. herein, the Debtors

launched an Asset Sale Offer, in compliance with the 1L Notes Indenture, on February 6, 2026.

The obligations under the 1L Notes Indenture are secured pursuant to that certain First Lien Security Agreement, dated as of August 8, 2024 (the “1L Security

Agreement” and, together with any other collateral documents purporting to secure the obligations under the 1L Notes Indenture, the “1L Collateral Agreements”), by and among Luminar, the Notes

Guarantors and the 1L Collateral Agent. Pursuant to such 1L Collateral Agreements, the 1L Notes are secured by a first lien security interest in substantially all of the Company’s and the Notes Guarantors’ assets.8 Additional information regarding the liability management and capital raising initiatives that resulted in the entry to the 1L Notes Indenture and 1L Collateral Agreements is set forth in

Section III.C.

| 7 |

On October 2, 2024, the Board approved the formation of a special committee to consider a potential acquisition of the Company as well as certain other transactions.

|

| 8 |

This includes accounts, equipment, goods, inventory, fixtures, documents, instruments, chattel paper, letter-of-credit rights, securities collateral, investment property and deposit accounts, intellectual property collateral, commercial

tort claims, general intangibles, money, supporting obligations, all books and records pertaining to any and/or all of the foregoing, all proceeds and products of each of the foregoing and all accessions to, substitutions and replacements